International SaaS payments are rarely solved by adding one more payment button. A SaaS company has to handle subscriptions, upgrades, trials, failed renewals, invoices, refunds, taxes, fraud checks, account access, revenue recognition, and customer support across multiple countries.

That is why the real question is not “Which payment provider is best?” It is “Which payment stack fits our SaaS model, markets, pricing, customers, and operational capacity?”

For some SaaS companies, cards and digital wallets cover most use cases. For others, bank transfers are still necessary for enterprise deals. Some teams need a Merchant of Record to reduce tax and compliance workload. Some international products can benefit from adding stablecoin or crypto payments for customers who cannot easily pay with cards, PayPal, or bank transfers.

This guide explains how to choose the right international payment stack for SaaS in 2026 without treating any single method as a universal answer.

Why SaaS international payments are different from e-commerce payments

A typical e-commerce payment ends after the order is paid, shipped, refunded, or disputed. SaaS payments continue for months or years. Every payment event can affect whether a customer keeps access to the product.

That changes the payment requirements.

A SaaS payment stack may need to support:

- Monthly, annual, and custom billing cycles

- Trials, coupons, upgrades, downgrades, and prorations

- Usage-based billing and prepaid credits

- Failed payment retries and dunning flows

- Enterprise invoices and manual payment approval

- Multi-currency pricing and settlement

- Tax calculation or tax compliance workflows

- Payment status updates inside the product

- Reconciliation between billing, finance, support, and analytics

International expansion adds another layer. Customers may prefer different payment methods by region. Cards may fail more often in some countries. Bank transfers may be trusted for enterprise contracts but too slow for self-serve signups. Currency conversion can reduce margins. Local regulation can affect what you can offer, how you onboard customers, and how you handle payment data.

A good SaaS payment stack should not only process money. It should protect access logic, reduce support workload, keep finance data clean, and give customers a payment method they can actually complete.

Start with your SaaS payment model

Before choosing providers, define how your SaaS product charges customers. The right stack for a $19 self-serve tool is different from the stack for a $50,000 annual B2B contract.

Self-serve subscription SaaS

Self-serve SaaS depends on fast activation. The customer chooses a plan, pays, and expects immediate access. Cards, digital wallets, local payment methods, and sometimes PayPal are common baseline options.

The main risks are failed payments, checkout friction, involuntary churn, and regional card acceptance issues. If customers are international, you also need to think about local currencies, payment method availability, and whether the payment experience feels familiar enough to complete without contacting support.

B2B SaaS with invoices

B2B SaaS often needs invoices, purchase orders, bank transfers, approvals, and finance-team workflows. The payment is slower, but the deal size can justify more manual work.

For this model, bank transfers and invoice-based payment methods may be unavoidable. The payment stack should support clean invoice IDs, payment matching, reminders, and reconciliation. If crypto or stablecoin payments are added, they should be tied to invoice status and finance operations, not treated as a standalone wallet transfer.

For a deeper comparison of bank rails and crypto rails, see the guide to crypto payments vs bank transfers.

Usage-based SaaS and AI/API products

Usage-based SaaS needs a different payment rhythm. Customers may top up balance, consume credits, replenish usage, and keep working without waiting for a monthly renewal date.

This model is common for AI tools, developer APIs, proxy platforms, infrastructure products, data tools, and GPU or hosting services. A prepaid balance can work better than trying to force every user into a traditional subscription.

Stablecoin or crypto payments can fit here when users already hold digital assets or need fast balance top-ups. But the product must handle payment status, underpayment, wrong networks, delayed confirmations, and balance crediting carefully.

Enterprise SaaS

Enterprise SaaS prioritizes procurement, contracts, legal review, payment terms, and internal approvals. Cards may be irrelevant for large accounts. Bank transfers, ACH, SEPA, SWIFT, and invoice workflows often matter more.

For enterprise accounts, the payment method is only one piece of the process. The bigger questions are contract currency, tax treatment, settlement, payment matching, and whether your finance team can reconcile payments without manual chaos.

Cards and digital wallets: the default, but not the whole stack

Cards are still the default online payment method for many SaaS companies. They are familiar, fast for the customer, and well supported by modern payment providers. Digital wallets built on card rails can also improve checkout speed because the customer does not need to type card details manually.

For SaaS, cards work well when:

- Customers expect instant self-serve access

- The product has monthly or annual subscriptions

- The market has strong card penetration

- The payment provider supports stored credentials and recurring billing

- Fraud, disputes, and failed payments can be managed with existing tools

Cards also come with trade-offs. International cards can have additional fees. Currency conversion can add another cost layer. Card disputes and chargebacks require evidence, internal workflows, and support time. Some customers cannot use cards reliably because of issuing bank declines, country restrictions, card limits, or local payment habits.

For most SaaS companies, cards should remain a core part of the stack. But global SaaS teams should avoid assuming cards will work equally well for every customer in every market.

PayPal and digital wallets: useful trust layer, uneven economics

PayPal can be valuable when customers recognize it and trust it more than entering card details on a new SaaS site. It can be especially useful for freelancers, small businesses, international buyers, and users who already keep a PayPal balance.

The trade-off is cost and control. Cross-border commercial payments can include extra percentage fees and fixed fees depending on country, currency, product, and account setup. PayPal can also introduce account holds, dispute processes, and regional restrictions that may not fit every SaaS model.

PayPal is usually strongest as an additional option, not as the only international payment method. It can improve trust for some customers, but SaaS teams should track whether it improves net revenue after fees, disputes, refunds, and support workload.

Local payment methods: conversion depends on geography

A global SaaS checkout should not look identical in every country. In some markets, cards are enough. In others, customers may expect bank debit, instant bank transfer, wallets, local payment schemes, or country-specific methods.

Local methods can improve payment completion because they match customer habits. They can also reduce some card-related issues, depending on the market and payment rail. But they add operational complexity. Each method may have different settlement timing, refund rules, failure modes, chargeback behavior, and reporting structure.

Local methods are worth considering when:

- A specific country or region is strategically important

- You already see card declines from that market

- Customers ask for a familiar local option

- The expected revenue justifies integration and support

- Your payment provider can route and reconcile those methods cleanly

Do not add local payment methods only because a provider supports them. Add them when they solve a real market problem.

Bank transfers: still important for B2B, weak for instant self-serve

Bank transfers remain important for international B2B SaaS, especially for larger contracts. Finance teams are familiar with them, invoices are easy to attach to procurement workflows, and some customers prefer bank rails for large payments.

But bank transfers are not ideal for low-ticket self-serve SaaS. They can be slow, hard to automate, and difficult to match when the customer forgets the payment reference. International wires may involve intermediary banks, unclear fees, delays, and currency conversion.

Bank transfers fit best when:

- Deal size is large enough to justify manual handling

- The customer is an enterprise account

- Payment terms are negotiated

- Finance teams need formal invoices

- The product can wait for payment before activation or renewal

They fit poorly when the product depends on instant activation, low-friction checkout, frequent top-ups, or automated renewals.

Merchant of Record: when SaaS teams want to outsource more than payments

A payment gateway processes payments. A Merchant of Record does more. Depending on the provider and agreement, a Merchant of Record can act as the seller of record and handle parts of tax collection, tax remittance, compliance workflows, chargeback management, and payment operations.

This can be valuable for SaaS companies that sell internationally but do not want to build a full global tax and compliance function early.

A Merchant of Record may fit when:

- You sell digital products or SaaS in many countries

- You need help with VAT, GST, sales tax, and local requirements

- You want one commercial layer across multiple payment methods

- Your team prefers higher fees in exchange for operational simplicity

- You do not want to manage local tax registrations alone

The trade-off is cost, control, and flexibility. MoR pricing can be higher than a direct gateway. Some providers may control checkout, billing rules, supported countries, payout timing, refund workflows, or account approval. For some SaaS teams, that is a good trade. For others, especially those with custom billing or complex product flows, a direct payment stack may be better.

The key decision is whether you want a provider that only processes payments or a provider that also takes on part of the commercial and compliance burden.

Stablecoins and crypto payments: when they fit international SaaS

Stablecoins and crypto payments are not a replacement for every SaaS payment method. They are an additional rail that can be useful for specific customer segments and payment problems.

For SaaS, crypto payments are most relevant when customers already hold crypto or stablecoins, card acceptance is weak in important markets, cross-border payments create friction, chargebacks are painful, or the product has a crypto-native audience.

Stablecoins such as USDT or USDC are usually more practical for SaaS than volatile assets because pricing, accounting, and customer communication are easier. A $99 plan paid in a dollar-pegged stablecoin is simpler to reconcile than the same plan paid in a volatile token.

Crypto payments can fit:

- VPN and privacy tools

- AI tools with prepaid credits

- Developer APIs and usage-based products

- Online education and digital products

- B2B SaaS with international customers

- Creator tools and paid communities

- Products serving customers in markets with payment restrictions or weak card acceptance

They fit poorly when customers do not understand wallets, refunds need to work like card refunds, compliance obligations are unclear, or the team cannot support wrong-network payments, gas issues, payment matching, and manual reviews.

For SaaS teams exploring this layer, the more focused guide on recurring crypto payments for SaaS goes deeper into renewals, top-ups, saved payment flows, and access logic.

The main crypto payment risks SaaS teams should design around

Crypto payments fail differently from card payments. A card payment may fail because the bank declines it, the card expires, or authentication is required. A crypto payment can fail because the user chooses the wrong network, sends the wrong amount, lacks gas, misses the invoice window, or sends funds that cannot be matched automatically.

For SaaS, those issues affect more than checkout. They affect activation, renewals, top-ups, account balance, support tickets, and customer trust.

The most common crypto payment risks are:

- Wrong network: the customer sends USDT on a network you do not support.

- Missing gas token: the customer has USDT but no TRX, ETH, BNB, SOL, or another native token required for the transaction.

- Underpayment: the customer manually sends less than the invoice amount.

- Late payment: the transaction arrives after the invoice expires.

- Unmatched payment: the payment arrives without a reliable link to the account or invoice.

- Unclear status: the user does not know whether payment is pending, confirmed, failed, or under review.

- Compliance hold: the transaction requires AML review before access or balance can be credited.

These issues should be handled in the product experience, not left for support to solve manually. The guide to reducing failed crypto payments is useful if your current flow relies too much on manual wallet transfers.

Network fees deserve special attention. Many users do not understand why holding USDT is not always enough to send USDT. If they lack the native token for gas, the payment may fail even though they have the funds. This is why gasless USDT payments and network fee abstraction matter for SaaS checkout and top-up flows.

Build the stack around costs, not just provider fees

Payment cost is not only the visible processing fee. SaaS teams should compare the full cost of each method.

The real cost includes:

- Processing fee

- International card surcharge

- Fixed transaction fee

- Currency conversion

- Settlement currency mismatch

- Refund cost

- Chargeback or dispute cost

- Fraud tooling

- Tax or compliance tooling

- Manual reconciliation time

- Support tickets caused by failed payments

- Engineering work for integration and maintenance

A method with a low visible fee can become expensive if it creates manual work. A method with a higher headline fee can be worth it if it reduces tax complexity, chargebacks, or billing operations.

For stablecoin and crypto payments, the cost model is different. There may be gateway fees, network fees, conversion costs, withdrawal costs, AML review costs, and support costs around user mistakes. Stablecoins can reduce volatility compared with BTC or ETH payments, but they do not remove operational risk.

Finance teams should define how funds are received, converted, held, withdrawn, reported, and reconciled. The guide to stablecoin payment operations for CFOs is the right next step for settlement, withdrawals, fees, and reporting.

If your main concern is price volatility, read the guide to protecting crypto payments from market volatility with stablecoins.

Integration checklist for CTOs and product teams

International SaaS payments should be integrated into the product lifecycle, not bolted onto the checkout page.

Before adding a provider, define the events your product must understand:

- Invoice created

- Payment started

- Payment pending

- Payment failed

- Payment expired

- Payment confirmed

- Subscription renewed

- Balance credited

- Access granted

- Access paused

- Refund requested

- Manual review required

- AML review completed

For cards and wallets, you need reliable subscription events, retry logic, payment method updates, webhooks, and customer notifications.

For bank transfers, you need invoice references, payment matching, manual review tools, and finance visibility.

For crypto payments, you need asset and network selection, invoice expiry logic, transaction detection, confirmation rules, underpayment handling, wrong-network handling, AML review, and clear balance or subscription updates.

A strong integration should make payment state visible to the product, finance team, and support team. No one should have to ask a developer to inspect logs or blockchain explorers to understand whether a customer has paid.

If the team needs custom control, a crypto payment API is usually the better path. If the goal is a faster launch with less engineering work, an HTML widget for crypto payments may be enough for a first version.

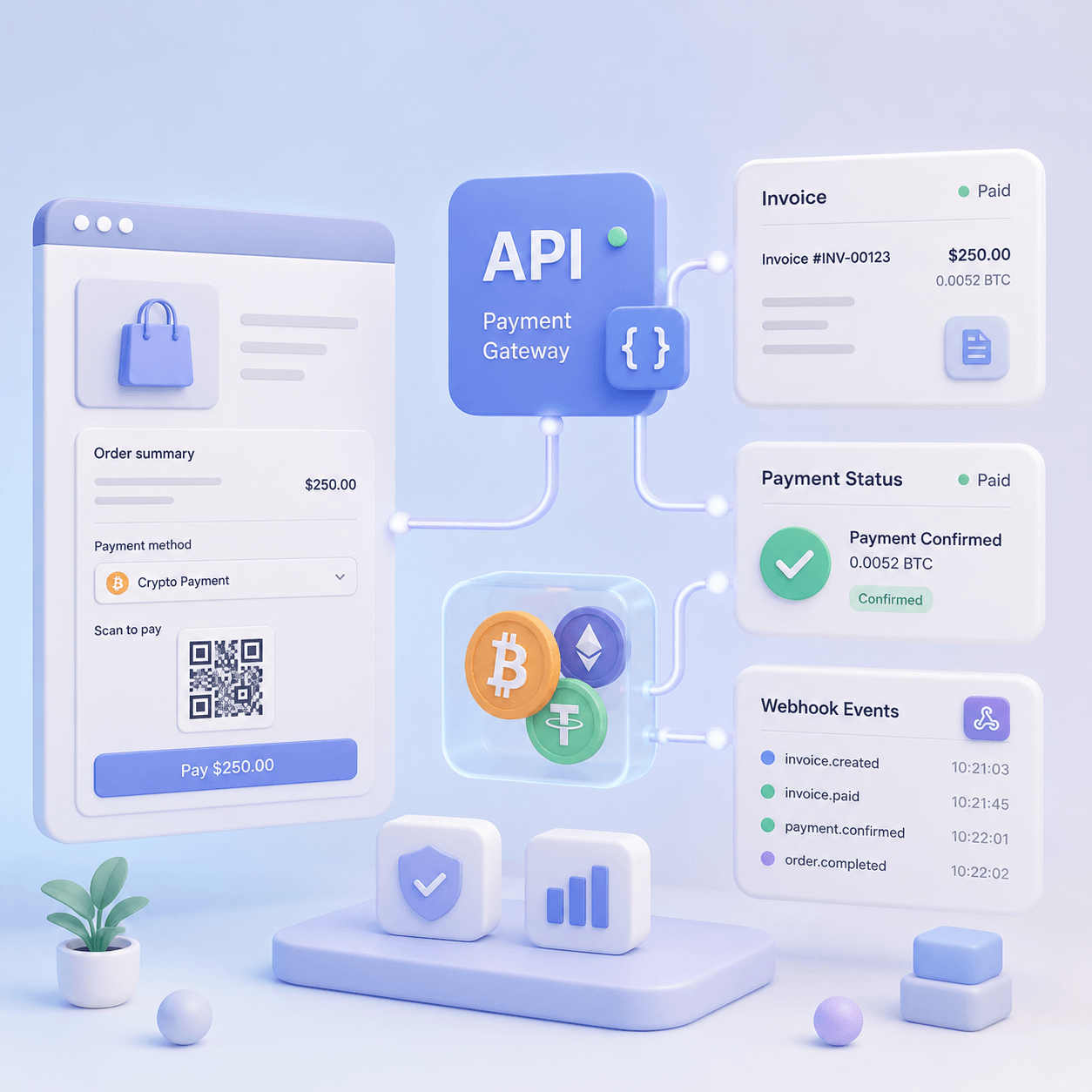

CryptumPay can fit this part of the stack when a SaaS business wants to add crypto payments on a website, in an app, or in another digital platform with API or widget integration, QR/app flow, USDT conversion, network fee handling, AML checks, and repeat payment flows after the first successful payment.

Compliance and regulation: do not treat it as a footer

International SaaS payments involve regulation even before crypto enters the stack. Cards, wallets, bank transfers, tax collection, data handling, fraud controls, sanctions screening, and refunds all have legal and operational implications.

Stablecoins and crypto add more questions:

- Which countries can you serve?

- Which assets and networks are allowed?

- Who performs AML checks?

- Do you hold customer funds or only process payments?

- How are refunds handled?

- What happens when a transaction is flagged?

- What records are kept for accounting and audit?

- Does your provider support the jurisdictions you care about?

There is no universal answer. Requirements depend on jurisdiction, customer type, product category, transaction size, custody model, and the exact role of your payment provider.

For European businesses or businesses serving European customers, the guide to stablecoin payments in Europe after MiCA is a useful starting point. It should not replace legal advice, but it helps frame the operational questions SaaS teams should ask before adding stablecoin payments.

How to choose the right SaaS payment stack

The best SaaS payment stack is usually layered. It gives most customers a familiar default option while adding alternative rails where they solve a real problem.

Use this decision flow.

1. Define your core revenue model

If you sell monthly subscriptions, optimize for recurring billing, retries, and payment method updates.

If you sell usage-based credits, optimize for top-ups, balance crediting, and fast payment confirmation.

If you sell enterprise contracts, optimize for invoices, bank transfers, payment terms, and reconciliation.

2. Map your customer geography

List the countries that drive current revenue and the countries you want to enter. Do not add every payment method globally. Add methods where they match buyer expectations and reduce friction.

3. Separate payment acceptance from payment operations

Accepting payment is only the first step. You also need settlement, reconciliation, support workflows, refunds, dispute handling, tax logic, and reporting.

A provider can have an excellent checkout and still create problems for finance if settlement and reporting are messy.

4. Decide whether you need a Merchant of Record

If international tax, compliance, and chargeback operations are becoming too heavy, a MoR can simplify the stack. If you need more flexibility, direct gateways and specialized rails may be better.

5. Add stablecoins or crypto only where they solve a clear problem

Crypto payments make sense when they improve access, reduce cross-border friction, support crypto-native users, reduce chargeback exposure, or enable faster top-ups.

They should not be added only because they look innovative. They should be added when they remove a real payment blocker.

6. Track performance by method

After launch, compare payment methods by business outcome, not just volume.

Track:

- Checkout conversion by country

- Payment success rate

- Failed payment reasons

- Refund and dispute rate

- Support tickets per payment method

- Settlement timing

- Net revenue after fees

- Manual reconciliation time

- Renewal recovery rate

- Top-up completion rate

- Share of customers using each method repeatedly

A payment method is successful only if it improves the customer experience and the operating model at the same time.

Example SaaS payment stacks

Early-stage self-serve SaaS

Start with cards and one accelerated checkout option. Add PayPal if your audience expects it. Add local methods only for priority markets. Consider crypto or stablecoins if your customers are international, crypto-native, privacy-conscious, or frequently blocked by traditional methods.

B2B SaaS with annual contracts

Use invoice-based bank transfers for larger customers, cards for smaller self-serve accounts, and a clear dunning flow for renewals. If customers in some regions struggle with bank wires or card payments, stablecoin invoices can be added as an alternative rail.

Usage-based AI or API product

Use cards for automatic billing where they work. Add prepaid balance for better cost control. Consider stablecoin top-ups if users need fast replenishment or already operate with USDT or USDC. Make sure access and balance updates depend on confirmed payment states, not manual support checks.

Global digital product or VPN

Use cards, wallets, and local methods where available. Add crypto or stablecoins for users who prefer wallet-based payments or face restrictions with traditional rails. Focus heavily on payment clarity: asset, network, amount, fees, confirmation status, and support instructions.

Final checklist before changing your payment stack

Before adding or replacing an international SaaS payment method, answer these questions:

- Which customer segment is this method for?

- Which country or corridor does it help?

- Does it support one-time payments, subscriptions, top-ups, or invoices?

- What are the visible and hidden costs?

- How fast is settlement?

- What happens when payment fails?

- What happens when a customer asks for a refund?

- How are disputes handled?

- How will finance reconcile payments?

- How will support understand payment status?

- What compliance checks are required?

- How will product access change after payment?

- Which metrics will prove whether the method works?

International SaaS payments are not a single-provider decision. They are a stack decision. Cards, wallets, local methods, bank transfers, Merchant of Record platforms, and stablecoins each solve different problems.

The strongest setup is usually the one that gives customers the right payment option for their context while keeping the business in control of access, settlement, risk, and reconciliation.

For many SaaS companies, that means keeping cards and traditional rails as the default, using bank transfers or MoR where they fit, and adding crypto or stablecoin payments as a focused alternative for international customers who need a faster or more accessible way to pay.